Asset quality concerns continue to plague India’s banks, especially those owned by the government, and analysts expect June quarter’s pain to remain in 2017-18.

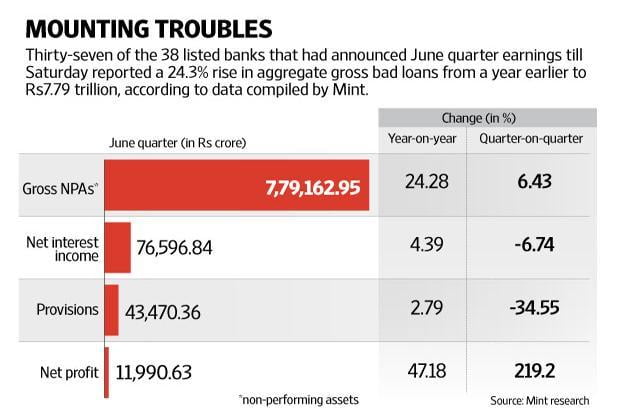

Thirty-seven of the 38 listed banks that reported June quarter earnings till Saturday have posted a 24.3% rise in aggregate gross bad loans to Rs7.79 trillion from a year earlier, data compiled by Mint shows.

The increase is 6.43% when compared with the March quarter. Of this, Rs6.83 trillion belong to public sector banks.

With a gross non-performing assets (NPA) ratio of 23.6%, Indian Overseas Bank tops the list, followed by UCO Bank with 19.9%.

“The first quarter numbers only underscore our stance that the bad loan problem will continue to exert pressure on earnings in this financial year,” said Saswat Guha, director, Fitch Ratings, which maintains negative outlook on the banking sector.

Besides corporate loans, there are concerns of potential slippages from the agriculture portfolio, following the announcement of farm loan waivers in several states.

The waivers contributed to higher bad loans in the first quarter for most lenders including HDFC Bank and State Bank of India (SBI).

So far, Uttar Pradesh, Punjab and Maharashtra have announced large-scale loan waivers and the cumulative debt relief stands at around Rs77,000 crore. Analysts fear that other states, especially those headed for elections, may follow suit.

Guha said there are incremental challenges from the announcement of farm loan waivers. Besides, power projects have become vulnerable as states seek to renegotiate power purchase agreements, he added.

Banks have also flagged emerging risks from the power sector loans.

In its first quarter earnings call on 25 July, Axis Bank said there is some stress in the power sector, outside its so-called watch list of stressed loans. Around 69% of the bank’s loan watch list of Rs7,941 crore is from the power sector.

At ICICI Bank, out of its watch list of Rs20,358 crore, the power sector accounts for Rs7,076 crore. More than a third of SBI’s watchlist of Rs24,444 crore is dominated by the power sector.

To be sure, leading banks have beefed up provisioning cover in the power sector and have included the potential impact on the balance sheet if bad loans from the power sector rise in their credit cost guidance.

However, on a sectoral basis, the overall recognition of stressed loans from the power sector is low and could lead to rise in provisioning requirement in case these loans turn non-performing, analysts said.

Given that the pool of stressed loans has not reduced, resolution remains a key factor, said Alpesh Mehta, an analyst at Motilal Oswal Securities.

“Everything is dependent on upgrades and recoveries, which are expected to improve in the second half of the year. Recoveries in the National Company Law Tribunal (NCLT) cases will be a key thing to watch out for, especially on the kind of haircut banks are going to take,” he said.

In case of agriculture loans, sector watchers are hopeful that once details of the schemes are out, there could be some revival. For instance, SBI is expecting a payout of around Rs3,000 crore from state government against loans waivers.

Apart from the poor asset quality, anaemic loan growth is also seen adding pressure on profitability, analysts said. Credit growth is seen weak because of lack of demand and the limited ability of public sector banks to grow due to capital constrains.

“Loan growth is not expected to recover much. State-owned banks are weakly capitalized and losing market share to private sector banks. It will be in poor single digit. Retail strategy of private sector banks is playing out very well because they have wherewithal in terms of capital and right set of people,” said Suresh Ganapathy, an analyst at Macquarie Capital.

Source:-livemint